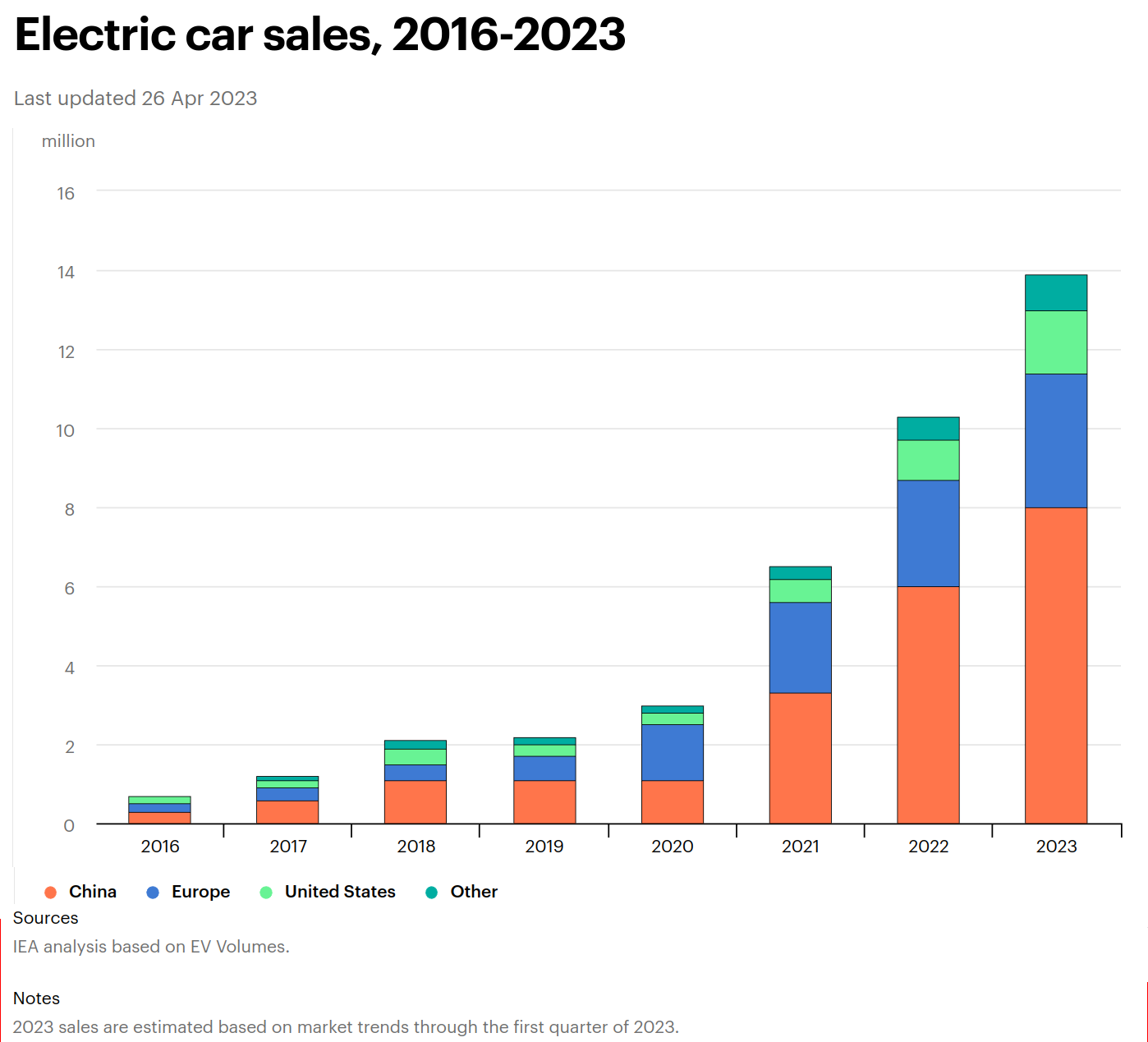

October's BEV Collapse Is Official: NADA Data Confirms the Tax Credit Hangover Was Real

The NADA Market Beat's October 31 report confirmed what analysts had been forecasting all month: BEV sales fell 46.7 percent from September and 23.8 percent year over year as the federal EV tax credit expiration delivered a historic shock to the US electric vehicle market.

The NADA Market Beat report, published on October 31, 2025, delivered the official confirmation that the automotive industry had been bracing for: battery electric vehicle sales in the United States collapsed in the first full month after the expiration of the federal EV tax credit. The data was unambiguous, and it confirmed that September’s surge was a pull-forward of demand rather than a genuine acceleration in EV adoption.

According to the report, BEV sales totaled 74,985 units in October — a decline of 46.7 percent from September 2025’s approximately 140,000 units, and a 23.8 percent decrease compared to October 2024. The market share math was equally stark: BEVs represented approximately 6.0 percent of new vehicle sales in October, down from an adjusted 9.1 percent in September and from 7.5 percent in October 2024.

The September Distortion

Understanding October’s collapse requires understanding what September actually was: a distorted data point, not a genuine reflection of market demand. The $7,500 federal EV tax credit, which had been available as a point-of-sale rebate since the Inflation Reduction Act’s passage, was always scheduled to expire at the end of September 2025 (for vehicles without a qualifying domestic content pathway that had been providing an alternative credit structure). For consumers who had been considering an EV purchase, the rational economic choice was to close the deal before the credit disappeared.

The result was an artificial surge in September EV sales across virtually every qualifying brand. Hyundai and Kia — whose Ioniq 5 and EV6 had been generating waitlists in 2024 — saw their highest monthly sales figures in September. Ford’s EV sales jumped 30 percent year over year. GM’s EV sales reached record quarterly volumes on the strength of late-quarter September deliveries. All of this volume was pulled forward from subsequent months, primarily October.

October’s numbers represent the market correcting for that distortion. The question the NADA data begins to answer — though a single month isn’t sufficient — is what the US EV market looks like without a universal financial incentive.

The Volume Brands Took the Biggest Hit

The brands most affected by the credit’s expiration were those that had relied on it most heavily as a competitive tool. Hyundai and Kia, which had positioned their strong E-GMP platform vehicles (the Ioniq 5 and EV6) against Tesla by emphasizing value and qualifying for the full credit, saw significant declines. Honda’s Prologue — a new entry in the EV market that was just establishing its sales trajectory — was also notably impacted.

Premium brands saw smaller percentage declines, partly because their customer bases are less price-sensitive and partly because several premium EVs — including those from Mercedes, BMW, and Audi — have been qualifying for the credit under the domestic assembly provisions. Tesla, which hasn’t qualified for the credit since early 2023, was effectively unaffected by its expiration.

The data raises a question that the industry has been reluctant to address directly: how many of the EVs sold in the 2023-2025 period were sold because of genuine demand, and how many were sold because of incentives? The October numbers suggest the ratio is uncomfortably close to 50-50 for some brands and vehicle types.

What the October Data Doesn’t Tell Us

One month’s data is not a trend, and there are important caveats to the October figures. The comparison to September is apples-to-oranges because of the credit-driven pull-forward. The year-over-year comparison, while more meaningful, is complicated by the fact that EV model availability, charging infrastructure, and consumer awareness have all improved substantially over the past 12 months.

It’s also worth noting that the $59,125 average transaction price for new EVs in October — up 2.3 percent year over year, per Cox Automotive — reflects the shift in sales mix toward higher-trim vehicles. The EVs still selling in volume without the credit are increasingly the ones buyers want badly enough to pay full price for. That could be read as either a sign of genuine demand resilience or as evidence that the lower end of the EV market is being strangled by the absence of affordability incentives.

The Policy Debate That October Ignited

The October data immediately reignited the policy debate about whether and how to restore EV purchase incentives. Ford publicly called for an extension of the credit in October, and several other automakers have reportedly been in discussions with policymakers about alternative structures — including point-of-sale rebates (which are more administratively efficient than the previous credit structure), fleet-focused incentives, and charging infrastructure funding.

Whether those discussions produce legislative results before the 2026 model year cycle — when several new affordable EVs from GM, Hyundai, and others are expected to arrive — is the key policy question for the US EV market’s near-term trajectory.

In the meantime, the NADA Market Beat’s October 31 report will stand as the definitive confirmation that the tax credit hangover was real, and that the US EV market’s path to mainstream adoption may be longer and more曲折 than the industry’s most optimistic projections suggested just 12 months ago.

Recommended Products

MotorLinks may earn a commission from qualifying purchases.